Campaign Flights

Campaign Name: Kenwood – Demystifying the Hard Money Loan Process for First-Time Investors

Blog Post

Demystifying the Hard Money Loan Process for First-Time Investors

The world of real estate investment can be both exciting and daunting, especially for first-timers. One term that often comes up, and might seem a tad intimidating, is “hard money loan.” If you find yourself puzzled by this concept, you’re not alone. This post will unravel the complexities of hard money lending and guide first-time investors through its intricacies.

1. What is a Hard Money Loan?

At its core, a hard money loan is a short-term loan secured by real estate. Unlike conventional loans, which are based on the borrower’s creditworthiness, hard money loans are based on the value of the property in question. This shift in focus makes them a popular choice for real estate investors looking for quick and flexible financing.

2. Why Choose Hard Money Loans?

Speed:

Traditional lenders, like banks, can take weeks to months for approval. Hard money lenders, on the other hand, can approve loans in mere days. This swift approval can be a game-changer in competitive real estate markets.

Flexibility:

These loans are typically more flexible in terms of requirements and conditions, making them ideal for unique properties or situations that might not qualify for conventional financing.

Short-Term:

Ideal for properties that investors plan to renovate and resell quickly. Hard money loans often have terms ranging from 12 months to a few years.

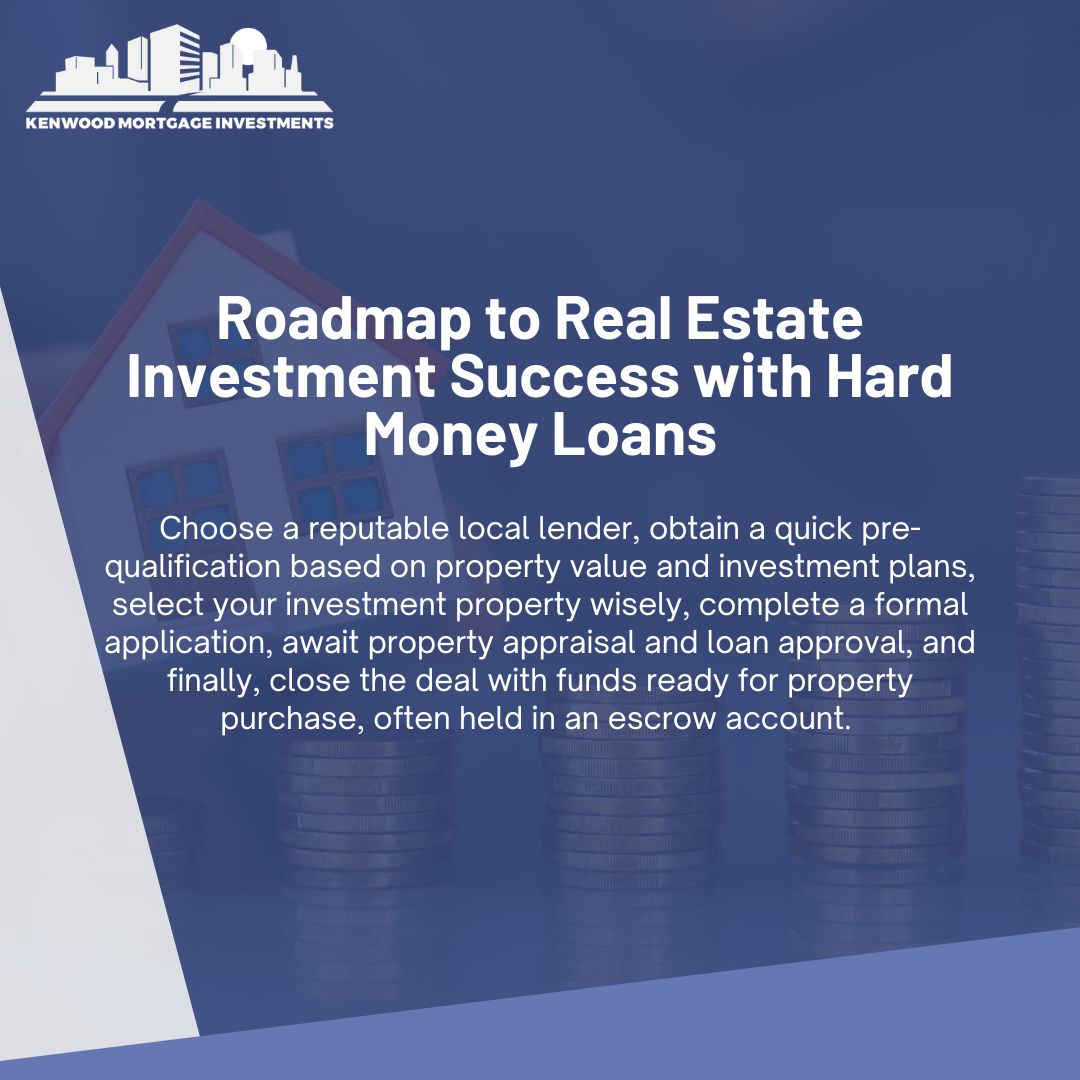

3. The Process Simplified

Step 1: Research and Choose a Lender: Look for reputable hard money lenders in your area, like Kenwood Mortgage, who understand the local market and have favorable reviews.

Step 2: Pre-Qualification: Much quicker than traditional loans, this step gives you an idea of what you might be approved for, based on the property’s value and your investment plan.

Step 3: Property Selection: Find a property you want to invest in. Remember, the loan amount will typically be based on its value.

Step 4: Formal Application: Submit your formal application, which will likely include details about the property, your plans for it, and some personal financial information.

Step 5: Appraisal and Approval: The lender will appraise the property to determine its value. Based on this, your loan can be approved and terms set.

Step 6: Closing: Once everything is in order, funds can be disbursed, often directly to an escrow account, to be released upon the property’s purchase.

4. Common Misconceptions

“Hard Money Loans are a Last Resort”: While they can serve those who might not qualify for conventional loans, they are often the first choice for savvy investors due to their speed and flexibility.

“Interest Rates are Too High”: While rates might be higher than traditional loans, the short-term nature of hard money loans means you might pay less over the loan’s lifetime.

“It’s Only for Experienced Investors”: Hard money loans can be perfect for first-time investors due to the flexibility they offer, especially for properties that need quick renovations.

In Conclusion

The realm of hard money lending doesn’t have to be shrouded in mystery. By understanding its fundamental principles and the process, first-time investors can confidently leverage hard money loans to catapult their real estate endeavors to new heights. So, if you’re considering your first investment, remember that hard money lending might just be the tool to set you on the path to success.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}